{kind=link}

Eurokai Shareholder Assembly in Hamburg

This week I did one thing I didn’t do for a while: I visited an annual shareholder assembly, on this case that of Eurokai in Hamburg. The primary cause was to get a greater impression of Tom Eckelmann, the sixth gneration household CEO who took over final summer season.

Other than the venue (Lodge Hafen Hamburg) with nice views over the harbour in Hamburg, these have been my foremost take aways (AGM presentation in German will be discovered right here) :

- Enterprise within the first 5 months is doing (a lot) higher than anticipated. That is the chart from the AGM displaying the quantity of containers:

The terminals in Marocco profit from the present challenge within the Suez canal. On high of elevated container throughput, they talked about that storage charges have elevated as nicely, because the delays from the Suez challenge require extra and longer storage and generate extra charges for port operators. Initially, Eurokai predicted a decrease end in 2024 in comparison with 2023, however they talked about that they could quickly change the outlook.

- New alliances: Gemini (Maersk & Hapag Lloyd)

An much more fascinating subject appears to be that the top of the Maersk / MSC Alliance and the brand new Hapag Lloyd / Maersk Aliance beginning in February 2025. If I understood that appropriately, 5 terminals of Eurokai will get the standing of a “Hub” for all Asian routes (Wilhelmshaven, Bremerhaven, Hamburg, Tanger & Damietta) which can doubtlessly improve visitors considerably going ahead. Maersk and Hapag Looyd don’t appear to go on to the Baltic harbours any extra and shift that visitors fully to the German ports. This was the chart they confirmed within the AGM:

General, Eurokai was fairly unconcerned in regards to the affect of the MSC funding into competitor HHLA. They count on that for the Hamburg terminal, the quantity that may shifted over from MSC will probably be greater than compensated from the rivals shifting quantity away from HHLA. For Bremerhaven, which Eurokai runs as JV with MSC, they count on no change.

General, my impression was fairly optimistic. To this point he appears to proceed what his father did. It will likely be fascinating to see if and when he will probably be setting his personal agenda.

General, issues at Eurokai appear to enter the correct route. I’ve already “recycled” the dividend into the inventory and may improve the place within the coming months.

Hutchison Port Holding Belief

As a result of it was on my to do checklist, I made a decision to look rapidly into Hutchinson Ports, the Port subsidiary of CK Hutchison. The primary have a look at TIKR’s overview web page reveals that now we have a really totally different firm right here in comparison with Eurokai:

The corporate seems to be extremely leveraged and the share value has misplaced nearly -90% during the last 15 years. Accorng to TIKR, Hutchison “solely” 27,6% and Temasek from Singapore round 16%.

Accoring to theri hompeage, the listed entity is simply a part of the complete Hutchison Ports Group:

It additionally appear to comprise solely Chinese language/Hongkong primarily based ports:

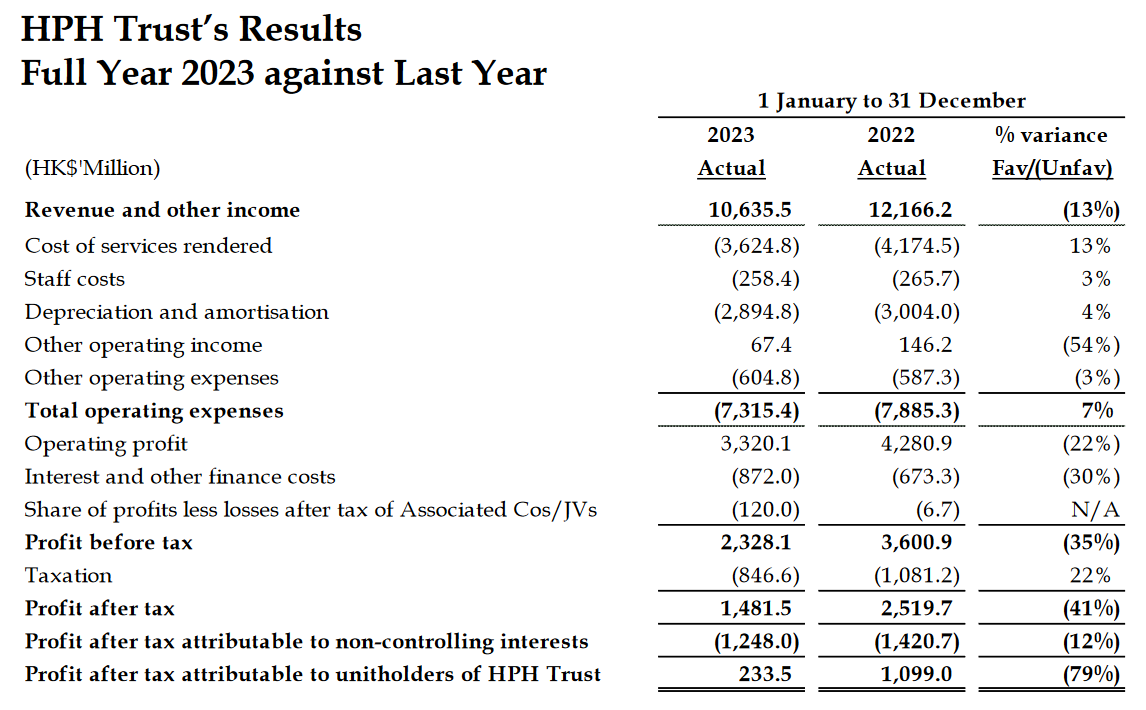

Financially, essentially the most related half in my view is the Money stream assertion which reveals that they distribute divdends that aren’t earned and that a lot of the earnings “evaporate” to minorities:

General, this clearly doesn’t appear like one thing I need to be concerned in.

The one fascinating side right here is that one can see “the opposite facet” of the enterprise kind the Eurokai ports. That is as an illustration what they wrote in Ferbuary:

So one may see this as an early indicator. Therfore I’ll attempt to learn the stories of Hutchson Ports kind time to time on how “the opposite facet” is doing.

P.S.: And naturally I used the journey to Hamburg for some “on website” Container terminal DD: