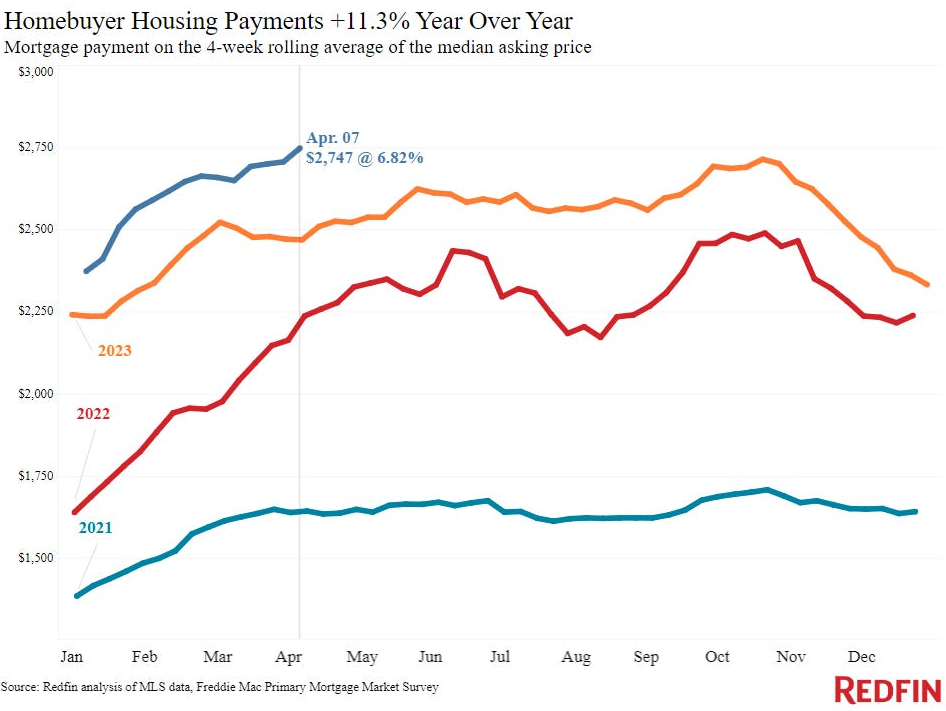

In keeping with Redfin, we simply hit one other new all-time excessive within the median month-to-month cost (based mostly on present dwelling costs and mortgage charges):

The median cost for a brand new buy has doubled since 2021.

Mortgage charges had been again as much as 7.4% this week. Nationwide housing costs are nonetheless are all-time highs and up round 50% for the reason that finish of 2019.

There was this sense of one thing has to present for some time now however nothing is giving.

All of which begs the query — who within the hell continues to be shopping for a home on this market?

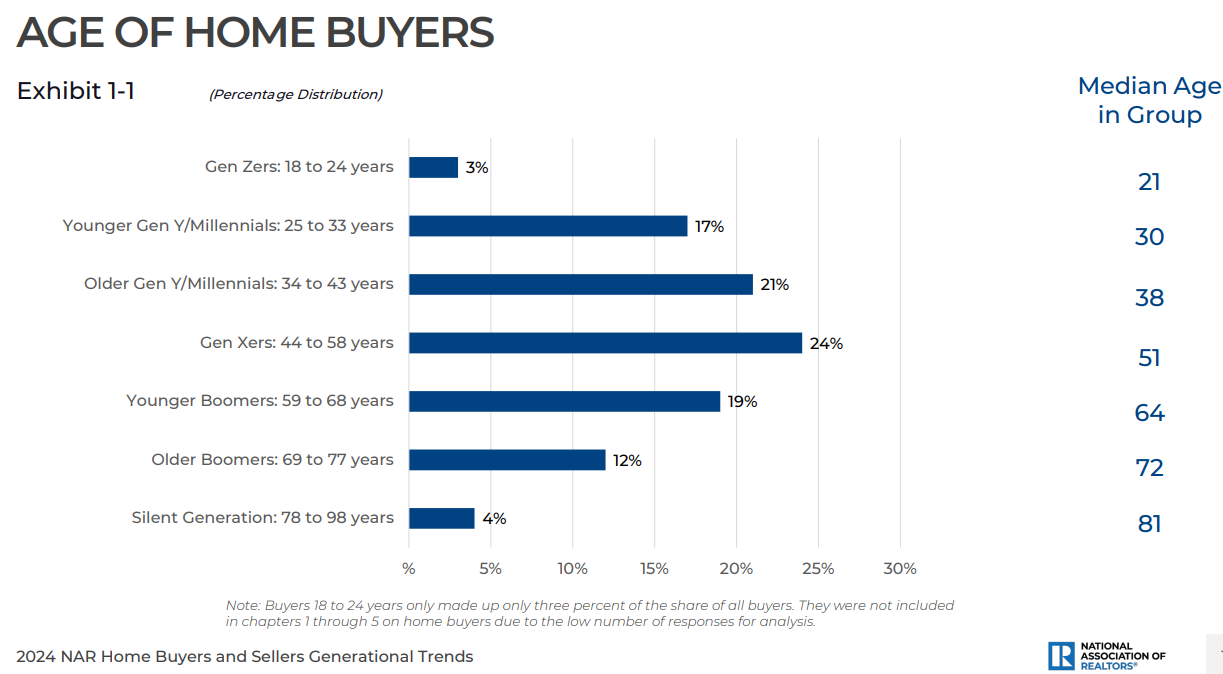

The Nationwide Affiliation of Realtors has the solutions of their newest House Consumers and Sellers Generational Developments Report.

Demographics are nonetheless within the driver’s seat. Millennials are the most important cohort of patrons with 38% of the whole:

Child boomers are subsequent according to 31% of purchases.1

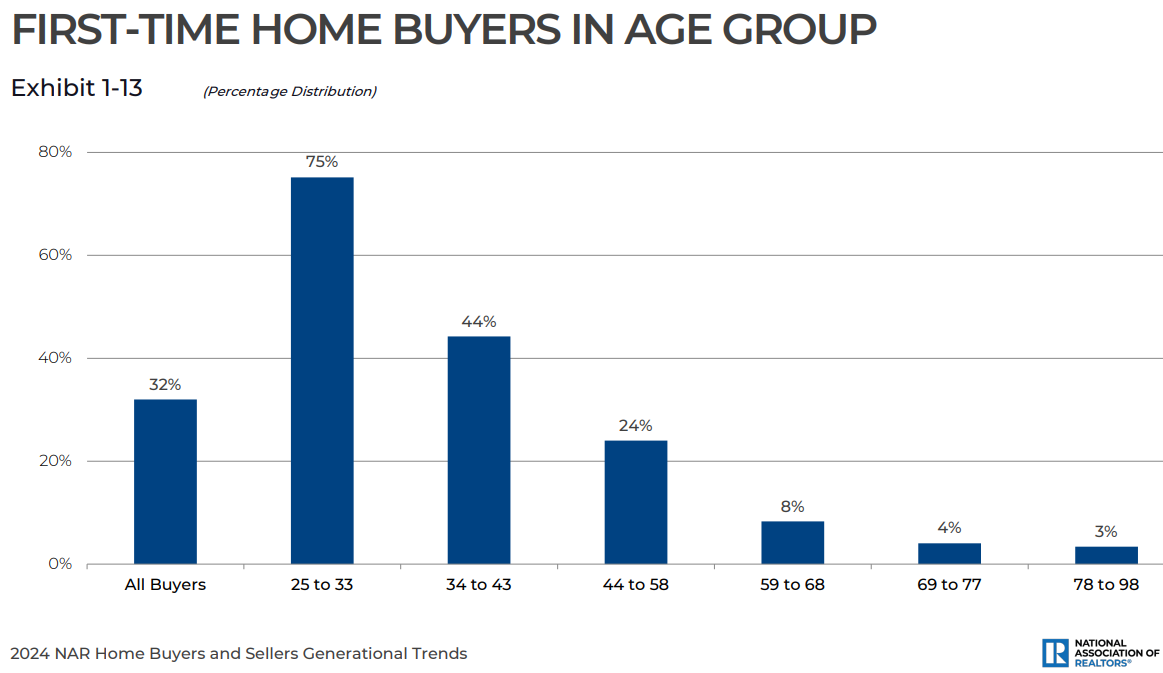

I do know it looks like it will be an not possible marketplace for first-time homebuyers however they make up three-quarters of the younger millennial cohort:

One-third of all patrons of late have been first-timers. Practically half of the 34 to 43 age group additionally bought their first dwelling.

To be honest, 24% of youthful millennials obtained some type of assist from a relative or good friend on the down cost.

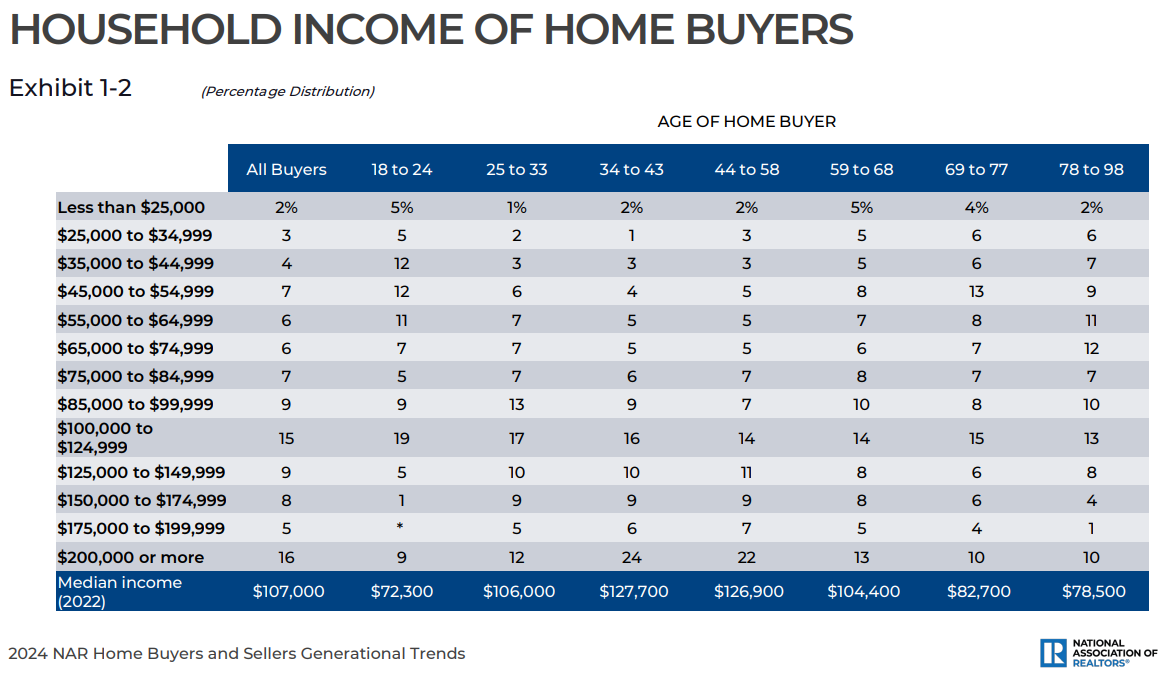

Right here’s a breakdown of patrons by earnings ranges:

Surprisingly, 44% of patrons make lower than six figures in earnings (which is actually the family median).

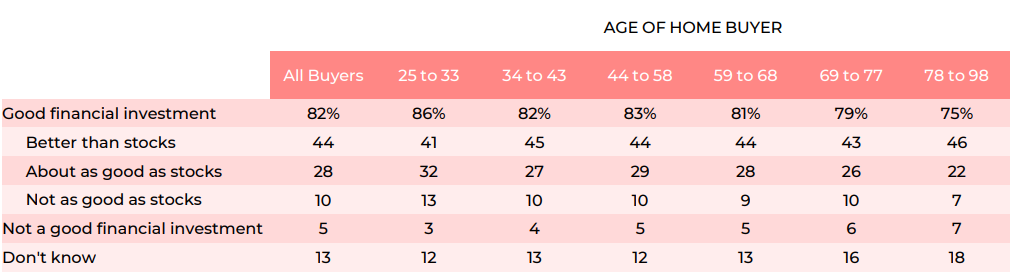

Most homebuyers nonetheless view housing as an excellent monetary funding:

Practically three-quarters of patrons assume housing is pretty much as good or higher than shares in the long term. My guess is inventory returns will likely be a a lot increased hurdle fee from present housing worth ranges, however who is aware of?

Greater than 70% of the homes bought had been constructed earlier than 2004, and greater than half had been constructed previous to 1988. If mortgage charges ever come down, there will likely be an enormous growth in HELOCs and cash-out refis, fueled by all of that pent-up dwelling fairness sitting in homes proper now.

I’m bullish on renovations for the rest of this decade.

It’s additionally value declaring that there are in all probability extra housing transactions occurring proper now than most individuals would assume, given the pricing and monetary dynamics.

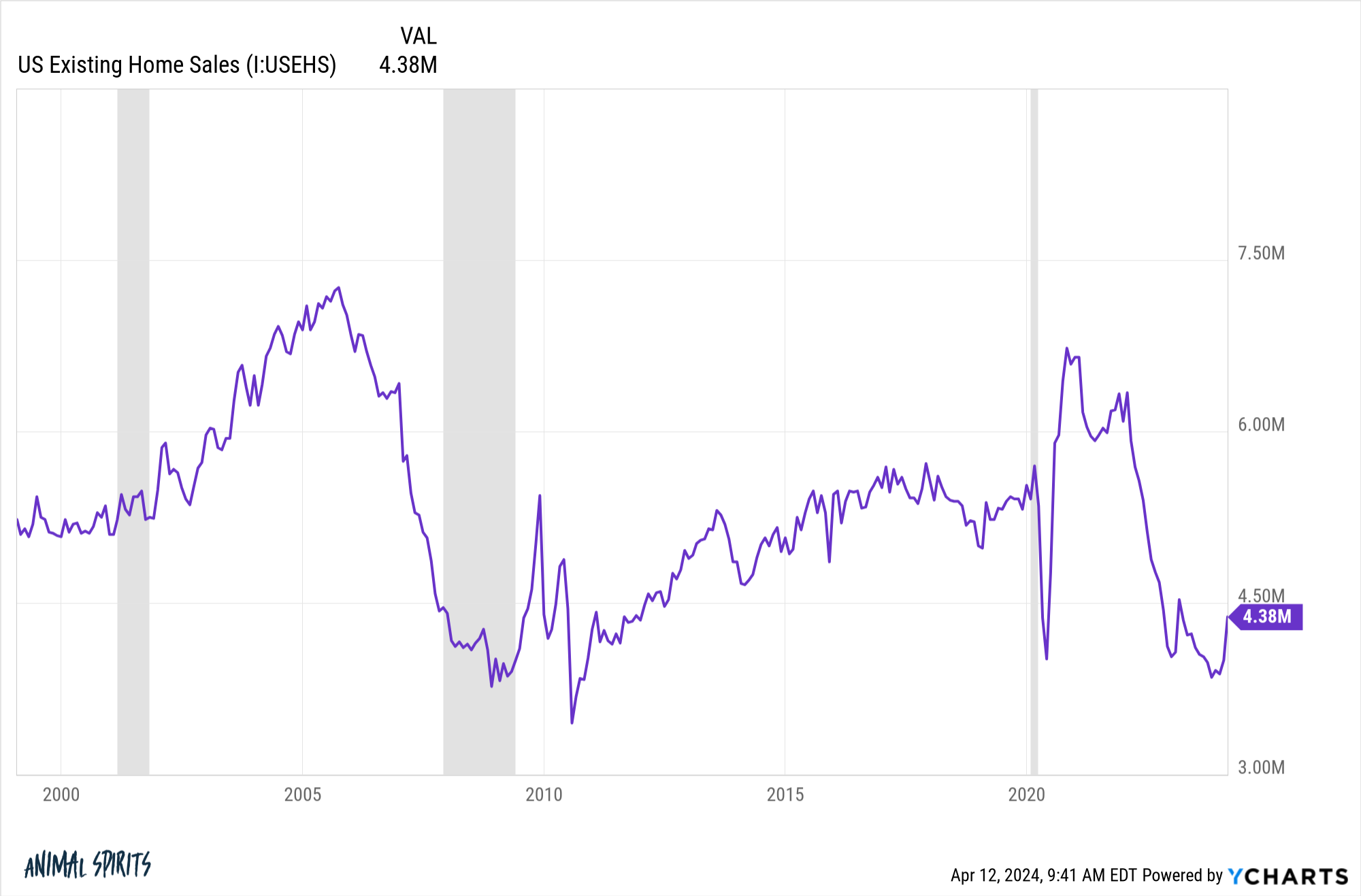

Right here’s a take a look at present dwelling gross sales:

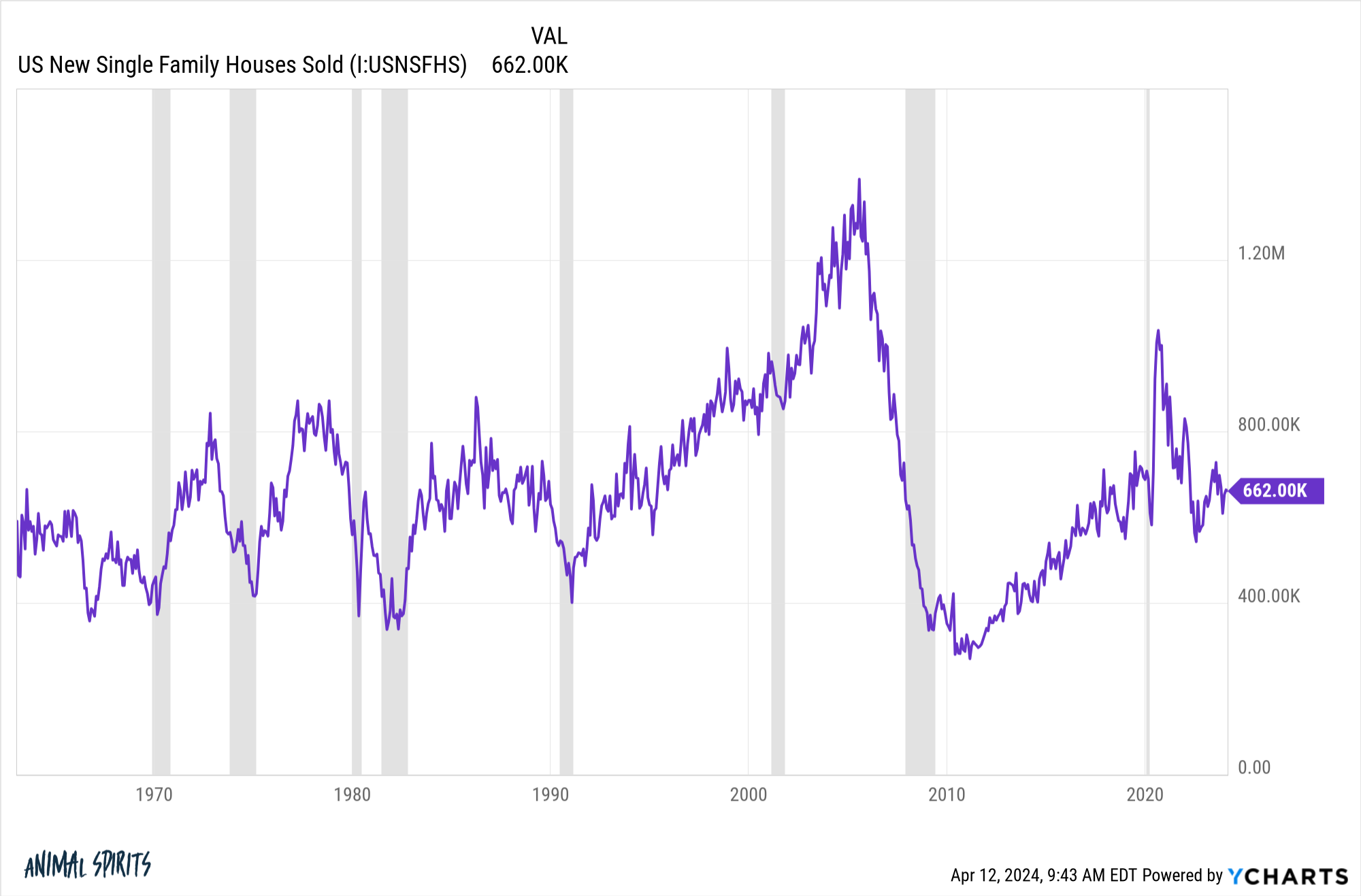

And new dwelling gross sales:

This information tells us there have been a bit of greater than 5 million homes bought prior to now 12 months. That’s down from round 6 million on the finish of 2019. So there was a lower in housing exercise however individuals are nonetheless shifting.

I do know which may not compute to lots of people who’ve finance on the mind, however it does make sense when you think about why individuals transfer or purchase a home within the first place.

There are 5 Ds of actual property — divorce, downsizing, diapers, diamonds, and demise — which drive individuals to purchase and promote. Add in new jobs and that covers many of the causes. Finally individuals have to maneuver as a result of life intervenes.

Folks change jobs. They transfer to a brand new metropolis. They get married. They begin a household. They get divorced. Somebody dies. Life goes on and other people make it work, excessive mortgage charges and all.

The excellent news is in case you can afford the cost now with mortgage charges so excessive you’ll be able to develop into it. Your wages will (hopefully) rise. You may refinance every time we do lastly have a recession or the Fed cuts charges.

The dangerous information is plenty of individuals merely can’t afford to purchase a house on this market. They don’t make sufficient cash. They don’t have wealthy mother and father who will help out with a down cost. Or they reside in an space that’s far too costly for patrons.

Sadly, the costly housing market is probably going going to make wealth inequality even worse than it already is.

However it’s additionally true that purchasing isn’t for everybody. For most individuals proper now, particularly these in huge cities, renting is much cheaper.

Simply ensure you purchase some shares because you’re not constructing any dwelling fairness.

Michael and I talked about who’s shopping for the entire homes, the boomer vs. millennial tug-of-war within the housing market and way more on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

Generational Luck within the Housing Market

Now right here’s what I’ve been studying these days:

Books:

1This can be a flip-flop from the final report when child boomers had been the most important patrons.