Firm overview

Bharti Hexacom Ltd. is a communications options supplier providing shopper cell providers, fixed-line phone and broadband providers to clients in Rajasthan and the Northeast telecommunications circles, which includes the states of Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland and Tripura. The corporate is providing providers underneath the model “Airtel”. It was initially integrated in 1995 as ‘Hexacom India Restricted’. In 2004, the identify was modified to ‘Bharti Hexacom Restricted’ when Airtel acquired a majority fairness curiosity within the firm. As of December 31, 2023, the corporate has its presence in 486 census cities and has an mixture of 27.1 million clients throughout each the circles. As of the identical date, buyer base included 19,144 thousand knowledge clients, of which 18,839 thousand have been 4G and 5G clients, and knowledge consumption per buyer per 30 days stood at roughly 23.1 GB through the 9 months ended December 31, 2023.

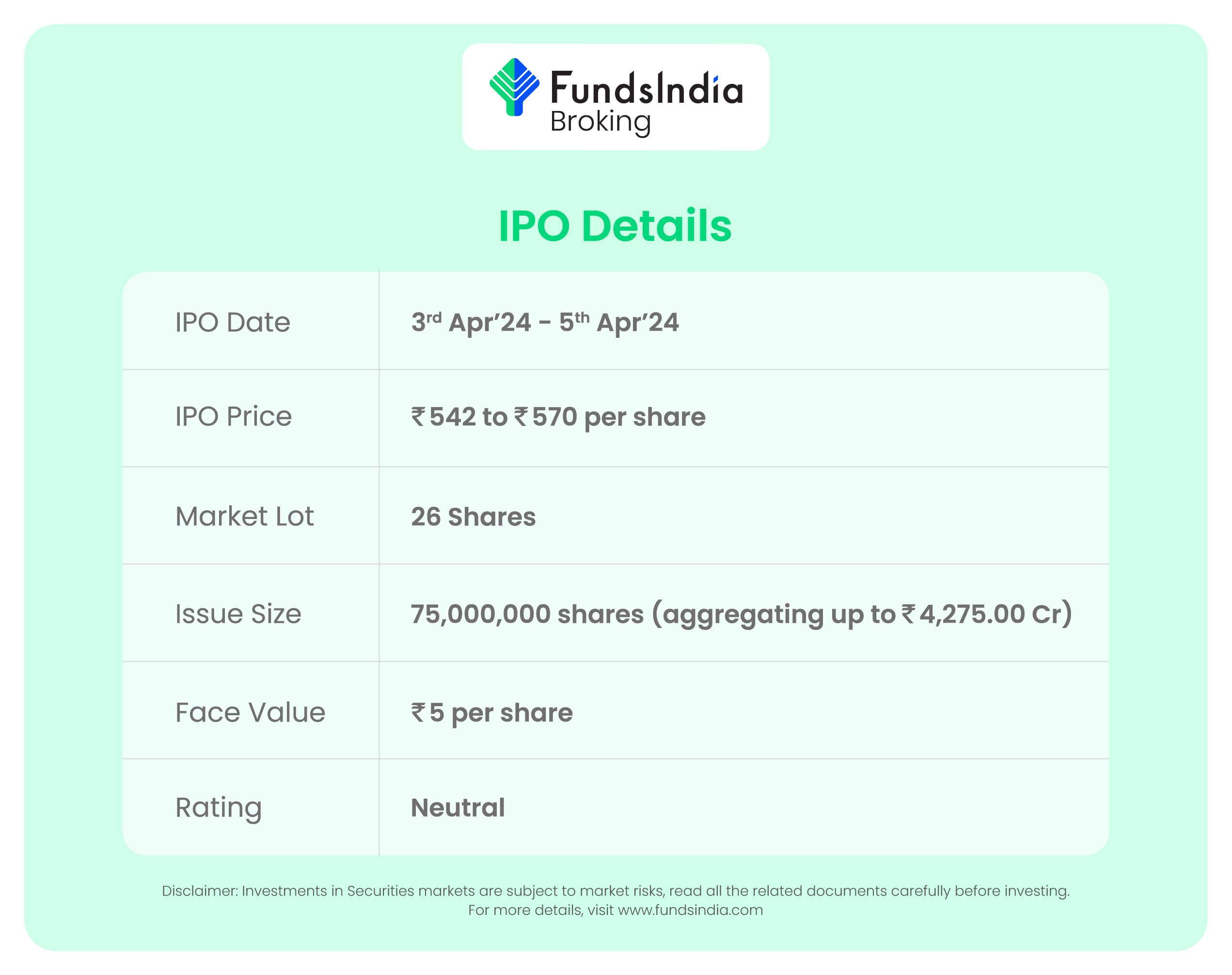

Objects of the provide

- Perform the Supply for Sale of as much as 75,000,000 Fairness Shares by the Promoting Shareholder.

- Obtain the advantages of itemizing Fairness Shares on the Inventory Exchanges.

Funding Rationale

- Sturdy parentage – The corporate is providing its providers underneath the well known model “Airtel”, which owns 70% stake within the firm. Airtel is a world communications options supplier with over 500 million clients in 17 international locations throughout South Asia and Africa. The corporate is deriving vital synergies from its relationship with Airtel and its associates, together with by Indus Tower’s infrastructure, inter circle roaming preparations, its nationwide long-distance community and company practical help.

- Established place –Bharti Hexacom’s income market share for Rajasthan and Northeast circle was 40.4% and 52.7% respectively throughout 9 months ended December 31, 2023, securing primary place in Northeast circle through the interval. The corporate is persistently enhancing its common income per person (“ARPU”) for cell providers from Rs.135 for FY21 to Rs.155 for FY22 to Rs.185 for FY23 to Rs.197 for the 9 months ended December 31, 2023. The corporate has the best variety of Customer Location Register – VLR (used to find out the variety of energetic customers on a cell community) clients (6.4 million) and a VLR market share of 52.3% within the Northeast circle and the second highest within the Rajasthan circle with 23.2 million clients and a VLR market share of 38.7%, as of December 31, 2023.

- Presence in markets with excessive development potential – The corporate operates in Rajasthan and Northeast circles in India which has excessive potential for growing the client base. Rajasthan’s buyer base is predicted to develop at 1.4% to 1.5% between FY23-28 reaching 69.0 million to 69.5 million with a teledensity of 82% to 83% following pan-India developments with rising rural teledensity. The shopper base within the Northeast is predicted to develop at 1% to 1.5% between FY23-28 reaching 13.2 to 13.5 million with a teledensity of 81 to 82%. Northeast circle telecom trade is predicted to develop at 6% to 7% between FY23-28 to achieve Rs.39 to 41 billion, supported by rising teledensity, greater web penetration and a possible improve in ARPU within the area.

- Monetary observe report – The corporate reported a income of Rs.6,579 crore in FY23 as in opposition to Rs.5,405 crore in FY22, a rise of twenty-two% YoY. The income has grown at a CAGR of 20% between FY2021-23. The EBITDA of the corporate in FY23 is at Rs.2,888 crore and EBITDA margin is at 44%. The CAGR between FY2021-23 of EBITDA is 59%. The PAT of the corporate in FY23 is at Rs. 549 crore and PAT margin is at 8%. The online revenue declined by 67% in comparison with the Rs.1,675 crore of FY22. The ROCE of the corporate stands at 10.72% in FY23.

Key dangers

- OFS threat – The IPO consists of solely an Supply for Sale of as much as 75,000,000 Fairness Shares by the Promoting Shareholders. All the proceeds from the Supply for Sale shall be paid to the Promoting Shareholders and the corporate is not going to obtain any such proceeds. The provide includes the sale of 75,000,000 shares by Telecommunications Consultants India Restricted.

- Geographical focus – The corporate derives its income from offering cell phone providers in Rajasthan and Northeast circle. The scope for development and buyer additions could also be restricted by restricted areas of operations. Any antagonistic developments in these circles may influence the corporate disproportionately in comparison with any of its rivals with pan-India presence. Challenges in establishing infrastructure services in these troublesome terrains (particularly in Northeast) and rural areas may have an effect on the turnover.

- Regulatory threat – Discount in income resulting from regulatory ceilings on pricing by TRAI, or owing to pricing strain, discount in ARPU, might have an antagonistic impact on the enterprise, monetary situation, outcomes of operations and prospects.

Outlook

The providers Bharti Hexacom Ltd. offers together with Airtel and its associates have aided the corporate in catering to the wants of shoppers and enabled the expansion in market share. In comparison with rivals, who might have operations throughout a number of circles, the corporate’s scope for development and buyer addition could also be restricted owing to restricted areas of operations in Rajasthan and Northeast. In response to RHP, Bharti Airtel Restricted and Vodafone Concept Restricted are the one listed rivals for Bharti Hexacom Ltd. The friends are buying and selling at a median P/E of 40.27x with the best P/E of 82.16. Vodafone is a loss-making firm and therefore it’s futile to compute its P/E. On the greater worth band, the itemizing market cap of Bharti Hexacom Restricted shall be round Rs.28,500 crore and the corporate is demanding a P/E a number of of 51.89x primarily based on submit challenge diluted FY23 EPS of Rs.10.98. When put next with its friends, the problem appears to be overvalued. Based mostly on the above views, we offer a ‘Impartial’ ranking for this IPO for a medium to long-term holding.

Different articles chances are you’ll like

Put up Views:

134