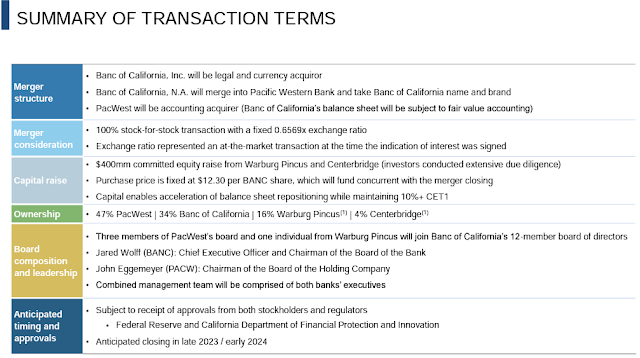

Banc of California (BANC) and PacWest’s (PACW) merger is a bit previous information at this level, however preliminary pleasure has worn off and shares are actually priced beneath $12.30/share, the place PE corporations Warburg Pincus and Centerbridge are making their PIPE funding (initially at a 20% low cost, it is going to shut with the merger). That is much less of a short-term particular scenario commerce and extra a medium-to-long time period funding as we look ahead to the skies to clear within the regional financial institution business and guess on the merged financial institution extracting an enormous quantity of synergies. The merger is a sophisticated transaction, the fundamental phrases are beneath, all of that is designed to scrub up the bigger distressed PacWest:

PacWest was one of many rumored subsequent dominos to fall on this previous spring’s banking disaster. Their technique was to make use of low price California deposits (together with a enterprise capital deposit clientele) after which lend these deposits out throughout the nation to CRE and business debtors. When their depositors fled, PacWest was compelled to load up on costly wholesale funding to plug the outlet. A part of the issue was their clients (each depositors and debtors) did not see them as their major financial institution, debtors weren’t depositors and depositors weren’t debtors. Banc of California contrastly operates extra like a big group financial institution, they collect deposits and lend in the identical geographic space, southern California.

The accounting right here might be a bit quirky, in an acquisition or a merger, a financial institution must mark-to-market the property of the acquired financial institution on their steadiness sheet. As everyone seems to be properly conscious, the place present charges are, banks have massive unrealized losses that are not included on their steadiness sheet in each the loans held for funding and securities held-to-maturity portfolios. Since Banc of California is in comparatively higher form, PacWest would be the acquirer right here in order that BANC’s property are marked-to-market somewhat than PACW’s. There’s a variety of shifting items right here (BANC is promoting their residential mortgage and multi-family portfolios amongst different asset gross sales to plug the wholesale funding drawback), however within the curiosity of brevity, Warburg Pincus and Centerbridge’s funding was designed to plug the capital ratio gap created by this mark-to-market merger accounting, holding the merged financial institution’s capital ratios within the wholesome 10+% CET1 vary.

My excessive stage core thesis right here is especially two fold:

- Pre-regional financial institution disaster, financial institution mergers have been extremely scrutinized. Again in the summertime of 2021, President Biden launched an government order that “encourages DOJ and the businesses chargeable for banking (the Federal Reserve, the Federal Deposit Insurance coverage Company, and the Workplace of the Comptroller of the Forex) to replace tips on banking mergers to supply extra sturdy scrutiny of mergers.” What this meant in observe, banks needed to persuade regulators/politicians to approve a merger by limiting department closures and job cuts, make grants into the group, and so forth. That is not the case right here, regulators are rolling out the pink carpet to make sure that the contagion does not unfold. The 2 events are guiding to solely a six month merger timeline as they’ve already previewed this cope with regulators. Whereas they’re going to watch out to not explicitly say it, however the two banks have a ton of geographical overlap that may get rationalized within the coming 12 months or two submit closing, probably blowing previous their projected synergies.

- Banc of California beforehand had a status as a little bit of a renegade quick rising financial institution below Steven Sugarman (brother of SAFE’s Jay Sugarman), they entered a variety of dangerous traces of enterprise and even plastered their identify on a brand new soccer stadium in LA for $15MM/12 months, fairly the advertising and marketing expense for a small regional financial institution. Nonetheless, 4 plus years in the past Sugarman was pushed apart, in got here Jared Wolff to steer the financial institution, he grew up at PacWest (with a cease in between at Metropolis Nationwide, one other LA financial institution) and is aware of it and its administration workforce very properly. Wolff shed most of the dangerous traces of enterprise, ditched the stadium licensing deal, as an alternative centered on being a group business financial institution. BANC has carried out fairly properly since, buying and selling between 1.1-1.4x guide worth. It is a little bit of a jockey guess that he can draw on each his expertise turning round BANC and being the previous president of PACW to merge these two organizations optimally.

By way of valuation, BANC put out the beneath estimate for subsequent 12 months’s EPS. It is a full 12 months view and never a run charge, one can assume the exiting run charge is probably going above this vary going into 2025.

Utilizing an admittedly pretty easy evaluation, however I believe it really works, utilizing the $12.30/share value quantity the place the PE corporations are coming in and the EPS steering mid-point of $1.72/share, BANC is buying and selling for roughly 7.2x subsequent 12 months’s earnings and even cheaper on a 12 months finish 2024 run charge foundation. The financial institution additionally gave a $15.13/share proforma tangible guide worth, or it’s at present buying and selling at 81% of guide, in comparison with traditionally round 1.1-1.4x. E-book worth does not embrace the mark-to-market losses on PacWest’s mortgage portfolio or held-to-maturity portfolio, however with a financial institution run largely off the desk, these losses will ultimately burn off. At 10x $1.80/share in EPS, BANC could possibly be a ~$18/share inventory by the top of subsequent 12 months.

Different ideas:

- This deal does not remedy two points the market has been frightened about, geographic focus and deposit focus threat, the mixed financial institution will nonetheless be business centered (missing vital retail deposits) and in California. However possibly neither needs to be a priority going ahead? Market could possibly be combating the final struggle, however one thing I have been eager about and do not have a robust rebuttal.

- One among BANC’s pitches is there’s a void to fill as a result of most of the largest California headquartered banks have both failed or been merged away in recent times. I do not fully purchase that as the cash middle banks have a big presence in California, banking is a relative commodity, whereas relationship group banking could be a good worthwhile area of interest, I battle considering there’s huge development alternative right here. It is a merger execution story, not a development one.

- Proforma, 80% of deposits might be insured, prefer to see {that a} bit increased, however it is a business centered financial institution. They will nonetheless be a reasonably small financial institution with solely 3% deposit share in southern California.

- Outdoors of the present financial institution surroundings dangers, this example does carry a good quantity of execution threat. I have been aside of some acquisitions earlier than, issues at all times take longer and are hairier than it seems to outsiders, have to have some endurance.

Disclosure: I personal shares of BANC and PACW