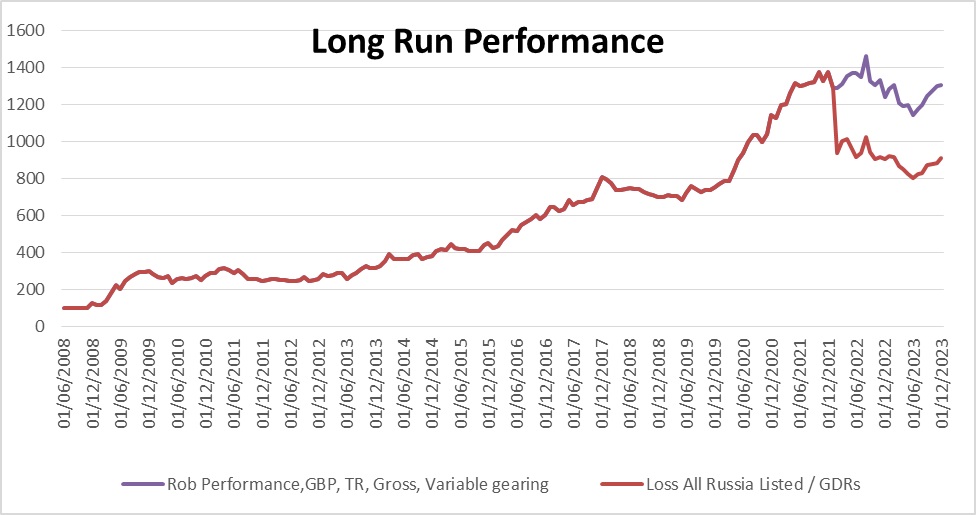

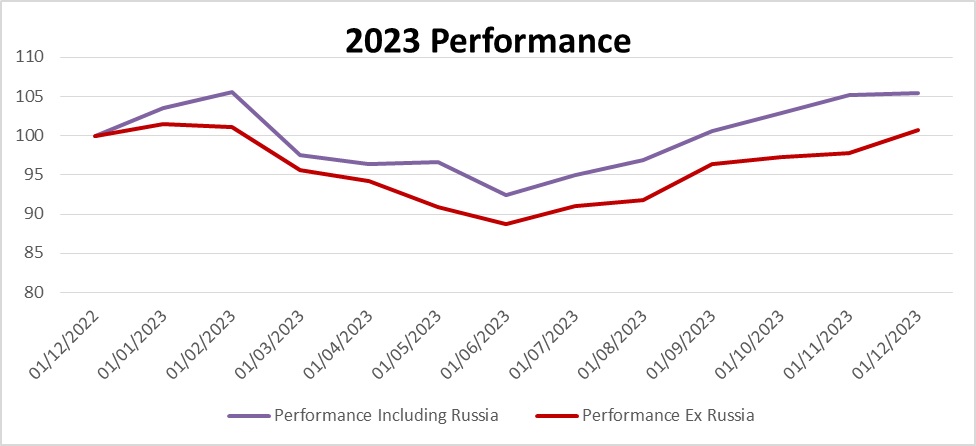

Normal finish of 12 months evaluation right here. It hasn’t gone nicely, general +0.8 (excluding Russian frozen shares) or +5.4% together with Russian frozen shares. If Russia goes again to regular can be up way more as there are a whole lot of dividends ready to be collected, not included within the under.

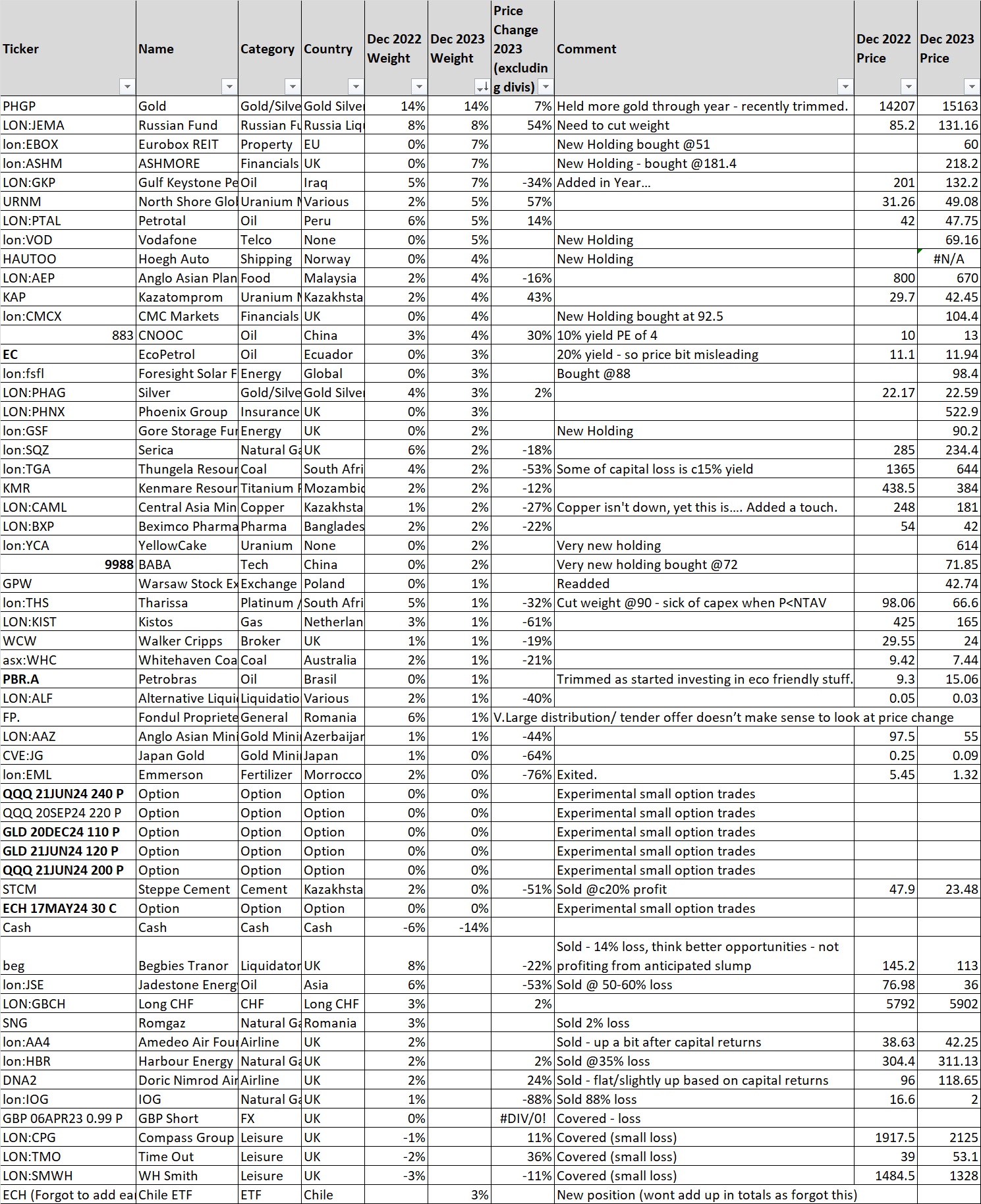

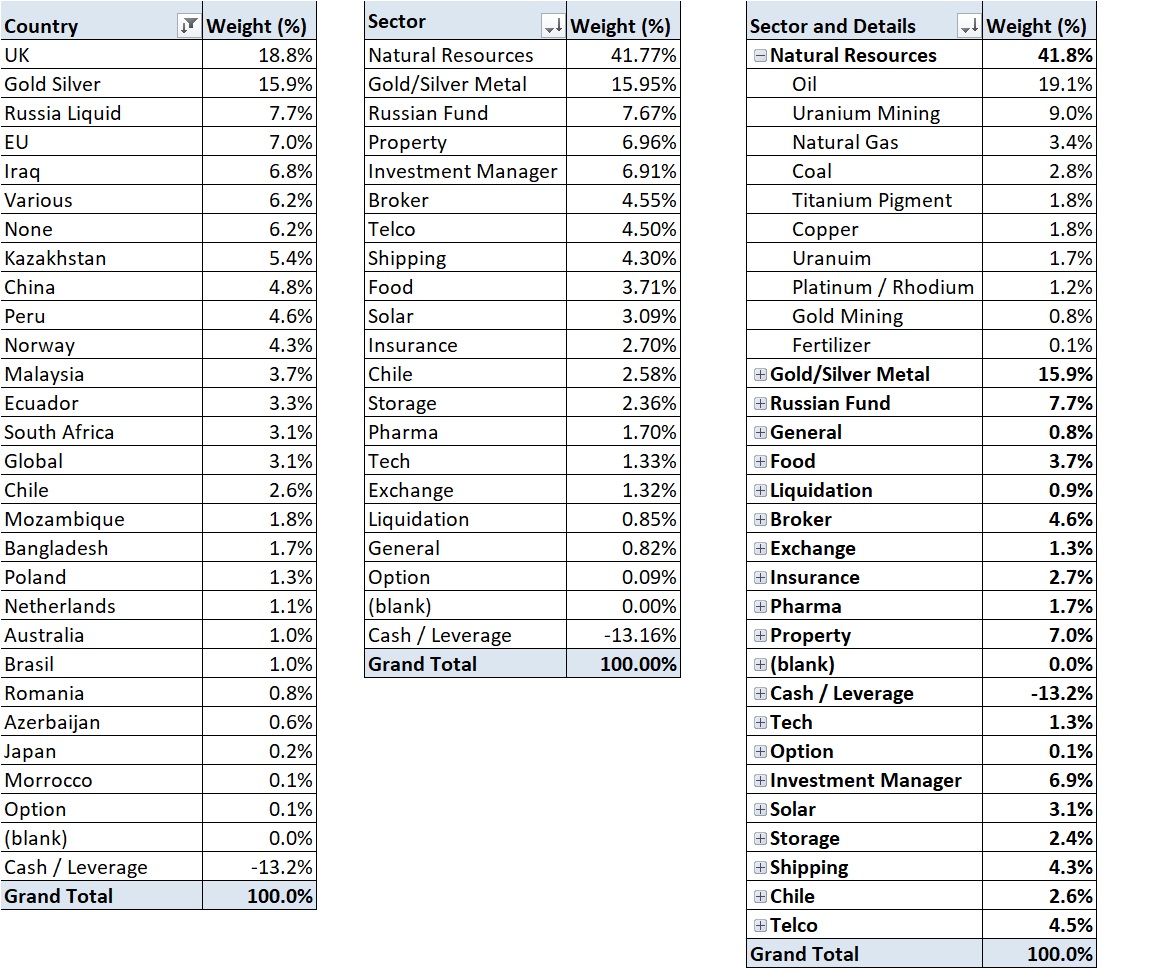

Linking again to final 12 months I used to be just about flawed about every little thing. I used to be closely into pure useful resource shares (c57% weight vs 41% now), not the most effective sector in 2023. Among the fall in weight is because of me mildly reducing weights as shares didn’t go my manner / although fairly a bit is because of worth falls. I had moments of excellent judgement – noticed the chance for political change in Russia – which very practically happened with the Prigozhin mutiny, received into financials late within the 12 months. Broadly issues haven’t labored. There’s a delicate optimistic ingredient to this – if I might be fairly flawed on virtually every little thing and nonetheless not lose *a lot* cash it’s not too dangerous – however it’s removed from superb given time I put in / potential returns. It’s additionally optimistic I havent gone off the rails after the big Russian loss final 12 months – its simple to chase / increase publicity, which is one thing I don’t assume I’ve completed. There’s an argument round stops – which I don’t use – going to be a bit of extra cautious with shares purchased at highs – significantly Hoegh Autos.

Weights are under:

Figures are as at twenty third Dec – so a bit of approximate – however a usually correct flavour of the place I’m. (some very illiquid shares like ALF costs are incorrect…

Not inclined to vary sector weights an excessive amount of, much less treasured about shares. I’ve additionally been fairly badly hit by manufacturing issues, AAZ had tailing dam points, PTAL – points with the natives, JSE – manufacturing issues. Undecided if that is simply dumb luck or a few of these issues have been within the worth – I actually knew PTAL had issues with ‘group relations’. JSE’s issues with their FPSO (floating manufacturing ship) may have been forseen if I had researched higher – vital to look into age of vessels, didn’t know/assume to do it on the time nonetheless. These few hundred million market cap shares are rather more susceptible than I assumed- money piles can evaporate in a short time in the event that they hit points.

Strikes in a few of my bigger weight useful resource co’s that I proceed to carry have been unlucky – CAML -27%, KIST -61%, TGA -53% and THS -32%. While gasoline and coal are down considerably copper is about buying and selling on the worth it was at the beginning of 2023, Tharisa’s basket isnt down that a lot. CAML is buying and selling at a PE of 8, 9% yield, THS PE of three.5, 1/4 e-book, although marred by a administration who insist on development capex while buying and selling sub e-book. They could get fortunate if costs rise however it’s luck, not judgement. TGA, additionally very, very low cost 7% yield, low single digit PE, once more, irritatingly, investing quite than returning capital. These giant falls should not smart from a capital preservation perspective, one wants a 100% rise to counter a 50% fall. But when we do get a choose up within the financial system / useful resource costs these may simply get again the place they have been. There may additionally be an argument these can simply rerate with the market, although at current they only appear to be disliked. PTAL appears to be doing nicely with respectable prospects and a ten%+ yield, with buybacks – all is dependent upon the oil worth. Draw back to all that is being commodity producers they solely have a lot management over their destiny – why many traders dislike them.

A inventory which has had manufacturing points is GKP – Gulf Keystone Petroleum it’s points concern the legitimacy of it’s manufacturing contract / pipeline entry. It’s the one one I’ve added to quite than diminished over the 12 months – averaging down. The entire Kurdish oil business has a query mark (relying on who you hearken to) relating to the legitimacy of it’s contracts. However, I can’t consider an instance the place a complete business was seized / nationalised / expropriated. Everybody – Kurdish govt / Iraqi govt and oil firms have stated that contracts can be revered / discussions are ongoing. It’s removed from danger free – I believe greatest danger is that one firm is punished / seized to encourage a deal to be made by the others. Enormous upside on this – it’s a really giant area with very low extraction price – regardless that the oil isnt the very best quality, if made reputable relying on the precise deal. They’re greater than overlaying their prices so in my opinion value a glance in case you have danger tolerance for a considerable loss. If this works it’s a 3x-5x or extra, however it’s one the place the result is essentially exterior administration’s management – for causes aside from commodity costs.

One among my greatest performing investments is JEMA – previously JP Morgan Russia. It’s an odd one – buying and selling at 48p ‘official’ NAV with a share worth of c £1.30 and a MOEX NAV at about £5-£6. JPM have marked all of the Russian holdings to about 0. I’m up about 55% and have trimmed the place – promoting a few third already. There’s rising speak of seizing Russian belongings to pay for the subsequent spherical of Ukraine funding. Not solely certain what to do on it – upside continues to be enormous however I have already got 30% of the portfolio worth in Russian, sanctioned shares. I dont actually need an additional weighting to turbo charged Russian publicity with the identical dangers – going to have to chop this to handle danger however considerably reluctant to, given the upside… I consider a whole lot of the frozen Russian belongings are held by Clearstream in Belgium , however uncertain to what diploma Belgium actually makes the decisons on that one. Russia seems to have ‘gained’ not less than to a point militarily – they’re making gradual progress, nonetheless they’re eager to have ‘peace’ / stop hearth talks. I believe it is because their wins should not sustainable, human losses/ monetary price is simply too heavy to be sustained. Ukraine lacks the manpower and probably arms for an ongoing attritional struggle however Russia lacks the motivation. My view is Russia cracks first and we see extra mutinies in 2024.

Uranium commerce has gone nicely – KAP/URNM up 43/53%. Have switched a bit of bit of cash out of URNM into YCA – perhaps the metallic will proceed to outperform the miners for fairly some time. I’m considerably skeptical of YCA / SPUT shopping for Uranium to tighten the market – as an industrial commodity – it solely actually has worth if it’s used – so implied worth of spot / spot -% means sooner or later will probably be used, and if will probably be used then tightening of the market most likely shouldn’t occur. Not how individuals are taking a look at it in the meanwhile although.

Financials have completed nicely – regardless of me including Nov/Oct in order that they haven’t had an excessive amount of time to contribute. October costs for many funding trusts / asset managers and so on. (principally UK based mostly) appeared very depressed, 10% yields 40% and so on low cost to e-book values. Startling how shortly issues have bounced. Not solely certain greatest technique to deal with these long term, they could possibly be a pleasant strong earnings play, purchased at excessive yields or if I discover one thing higher then time to promote . I wrote about these not too long ago in this publish. I’m a bit involved about them as a long term maintain – the upside may be very a lot restricted, although excessive chance. I desire to be within the ‘actual’ inflation linked financial system, arduous belongings quite than the monetary financial system.

A monetary I purchased after that publish is PHNX – Phoenix Group – it is a giant closed life insurance coverage supervisor it’s buying and selling at an honest 9% yield. The dividend is £500m for a corporation which is producing £1.3-1.4bn pa in money and which has £3.9bn solvency 2 surpulus – it needs to be sustainable. As ever with hyper large-cap insurers as an beginner you might be by no means fairly certain what the regulator will provide you with which can smash your day. You’re additionally betting towards the brand new weight reduction medicine growing lifespan – although of late expectancy has been falling unexpectedly. Not one I’ll maintain for too lengthy – I’m fascinated about a 12 months or two, however I believe it’s under-priced. Looking for alpha write up right here (not by me).

Bought out of AA4 and DNA2 – respectable income on each (+100% on some tranches, held since 2020) however I believe there are higher locations for funds now. I could also be lacking out on a little bit of upside if the A380 finds extra of a market – maybe if one other airline begins utilizing it, although I doubt it’s logistically easy. There at the moment are higher alternatives on the market, although AA4 might have extra upside however at greater danger.

Fondul Proprietea is now a tiny weight – after tender presents / returns of capital. Its a bit of unhappy to be saying goodbye. I got here up with this concept again in 2012 and have benefited from a closing of a 50% low cost and development in underlying investments – it’s actually the perfect funding. It has had a 962% rise since inception (2011) and I’ve owned it since 2012 – although once in a while have needed to drop it on account of dealer points. Time to promote this – as there isn’t an excessive amount of upside left now. Actually struggling to seek out issues with this stage of high quality / cheapness / ongoing compounding alternative.

Having stated this, one which can match the invoice is Beximco (BXP) it is a Bangladeshi Pharma, buying and selling at a PE of 5, doubled income since 2018 (in BDT, however even in USD it has grown impressively) and it has considerably elevated earnings (my 2019 write up right here). It’s at present buying and selling at half the place it’s in Bangladesh however there isn’t a arbitrage alternative. Frustratingly, I needed to minimize my weight as my dealer wouldn’t permit it in a tax environment friendly ISA account, this didn’t damage me as the worth fell. My dealer has modified their thoughts so now I can put it again and lift the load. Brokers right here appear to depend on giant screening corporations and drop / add corporations to the checklist of what’s eligible – not relying on the foundations however how they really feel on the time.

Walker Cripps may be very a lot the worst form of worth funding – the one the place nothing occurs. Walker Cripps is reasonable on an AUM foundation however hasn’t moved since I purchased it in 2015. Probably I’ve given this too lengthy, then once more there’s consolidation within the sector and this is able to be good for it… The FOMO of figuring out the day I promote it a suggestion can be made at 3x the present worth retains me holding, my not insubstantial endurance is working out.

I nonetheless have some leverage – however that’s low cost mortgage / unsecured debt at 3/4% charges. Its a comparatively small quantity vs portfolio / portfolio + property belongings – about 20%/11%. In impact, as in prior years leverage is getting used to purchase gold / held on deposit at a better charge…

By way of life – no change, nonetheless dwelling within the UK, quite unhappily employed (low/mid stage knowledge analyst) three days per week, doing investments / little little bit of property the remainder of the time. Actually wanting ahead to life beginning correctly when I’m now not employed / ideally leaving the nation. Was considerably distracted by a pointless courtroom case in the course of the first half of the 12 months and didn’t see a lot alternative so didn’t do a lot. Second half has been higher, significantly after October. I nonetheless assume a giant transfer in lots of the useful resource co’s I maintain is probably going, so actually dont wish to transfer earlier than that occurs – as a rustic transfer will entail pulling fairly a bit out of shares. PE’s of beneath 5 should not probably in my opinion to be sustained, although there’s a danger a sustained recession / despair shrinks earnings and share costs additional… I’d prefer to get extra copper / tin / silver publicity however haven’t but discovered any shares I like, and ETF’s should not with out their issues…

Suppose this 12 months has suffered from me principally being in respectable shares when it comes to yield / valuation however not shares the market cares about / likes which is why they’re low cost. I may go extra mainstream however I’d quite keep the place I’m and look ahead to the market come to me quite than chase… Not wedded to explicit shares however the weighting to the useful resource sector wants to stay – they’ve been beneath invested in they’re low cost and retro – very a lot assume they’ll have their day within the solar. Plan to change again from a number of the funds to sources as soon as the financials get again to nearer to what I anticipate is their honest worth.

Shares I plan to have a look at subsequent are tobacco – BATS/IMB most likely – if I can get comfy with authorized dangers / debt ranges, they’re yielding nicely and should not extremely valued. After I should purchase mainstream shares at single digit PE/ EV/EBITDA there isn’t a have to go too far into unique territory. Not the preferred – they do kill their prospects in any case, however vapes, hashish and so on might present a possibility to really purchase development at a low worth – significantly if regulation cuts out dodgy Chinese language imports. Nonetheless wish to rebuy Royal Mail on the proper worth. Long run I need extra Latin American / Asian listed shares. China seems to be low cost however I’m very cautious of avoiding a repeat of the Russian scenario.

Better of luck for 2024 – as ever feedback/views appreciated.